|

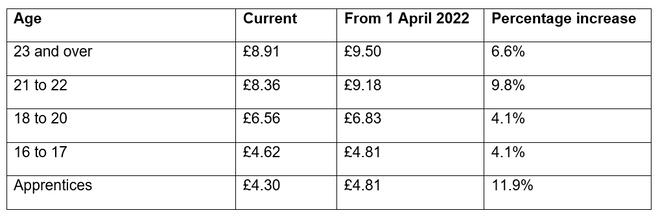

From 1 April 2022, the rate of National Living Wage paid to workers aged 23 and over will rise by 6.6%, or 59p, to £9.50 an hour. Apprentices will benefit from an 11.9% uplift to their current hourly rate of National Minimum Wage. For full-time workers, the 59p increase equates to extra annual salary of at least £1,000. Current and future rates of National Living/Minimum Wage are:  Apprentices receive the apprentice rate if they are either aged under 19 or in the first year of their apprenticeship. For example, a first-year apprentice aged 21 can be paid the apprentice rate.

The provision of accommodation is the only benefit that counts towards national minimum pay, with the maximum offset increasing to £8.70 a day (£60.90 a week). Common misconceptions HMRC has published a checklist of common causes of minimum wage underpayment:

National Living/Minimum Wage rates should not be confused with the Real Living Wage. This is independently calculated to reflect the cost of living and can be paid by employers on a voluntary basis; nearly 9,000 employers do so. The current Real Living Wage rate is £9.50 an hour, with a London rate of £10.85. It is aimed at all workers aged 18 or over. HMRC’s checklist of common causes of minimum wage underpayment, along with links to detailed guidance, can be found here.  For disposals of UK residential property completed on or after 27 October 2021, the reporting and capital gains tax (CGT) payment deadline has been extended from 30 days after completion to 60 days.

The previous 30-day time limit has proved to be quite challenging for taxpayers. For UK residents, the government has clarified that where a gain is made on the disposal of a mixed-use property, the 60-day time limit only applies to the residential element. Non-residents The new deadline also applies to non-UK residents who have to report and pay CGT on the disposal of any type of UK property, whether it is residential or commercial. Non-UK residents have faced particular problems because a Government Gateway login is required in order to set up a CGT on UK property account. Activation codes are sent by post, so they are often received outside the 30-day time limit. The alternative means having to complete a paper reporting form. The extra 30 days to report and pay should help but setting up a Government Gateway could still be problematic for those living overseas. Ongoing issues One of the biggest ongoing issues is that taxpayers are simply not aware of the reporting and CGT payment requirement when they make a property disposal.

If you believe you are affected, please get in touch with us as soon as possible so we can help you process your requirements. The start point for reporting and paying CGT on UK property can be found here.  Larger employers can transfer up to 25% of their annual apprenticeship levy pot to support other, smaller, employers to take on apprentices in England. While there is nothing new about this, what is new is an online service where funds can be pledged by larger employers. Apprenticeship levy funds are lost if not used within 24 months, so transferring surplus funds is obviously more rewarding than losing them. Pledging With the new service, the pledging employer simply uses their apprenticeship service account to create a transfer pledge. This will specify the amount of funds available for the current financial year. They can then choose four optional criteria to reflect priorities for transferring funding. These are:

At the time of writing, there were 45 funding pledges listed on the new online service, ranging from £1,618 up to a maximum of £342,263 – some without any criteria. Apprenticeships The benefit for smaller and medium-sized employers receiving a transfer of funds might not be as beneficial as it appears, because, for up to ten new apprenticeship starts each year, the employer only pays for 5% of the apprenticeship fees (and nothing if they have less than 50 employees). However, a transfer will remove the 5% cost, and the full cost if the ten-apprenticeship limit is exceeded. Although any employer can receive a transfer, they will need to set up an apprenticeship service account.

The current list of funding opportunities can be found here. |

Photos from Pam loves pie, Homedust, wuestenigel, Patrick Cannon Tax Barrister, wuestenigel, Brett Jordan, wuestenigel, raisin_raisin, wuestenigel, SME Loans, Alexandre Prevot, Jirka Matousek, wuestenigel (CC BY 2.0), wuestenigel, Jirka Matousek, moneybright, aronbaker2, foundin_a_attic, QuoteInspector.com, wuestenigel, Kate#2112, Semtrio, Rawpixel Ltd, itmpa, GoSimpleTax, DPP Law, UC Davis College of Engineering, 401(K) 2013, REM Photo ~ Sketchy Internet, Chris Yarzab, focusonmore.com, focusonmore.com, willbuckner, EpicTop10.com, Tony Webster, wuestenigel, B Rosen, London Less Travelled