By setting up an online childcare account, you can get a government top-up to help with the costs of childcare. However, thousands are missing out on this payment.

Tax-free childcare is worth up to £500 every three months (£2,000 a year) for each of your children, which doubles if a child has disabilities. Despite the impact of lockdowns, nearly 250,000 families saved money using the scheme in December 2020, an increase of more than 40,000 compared to a year earlier. How tax-free childcare works Your child must be aged under 12, with eligibility ceasing on 1 September after their 11th birthday (under 17 if a child has disabilities). For every £8 you pay into your childcare account, the government will pay £2. These amounts can then be used to pay for approved childcare, such as:

You can only get help paying for care outside of normal school hours, so, for example, private music lessons during school hours don’t count. Money can be saved during term time, earning the government top-up, and then used for summer camps or play schemes during school holidays. Restrictions There are certain restrictions on eligibility:

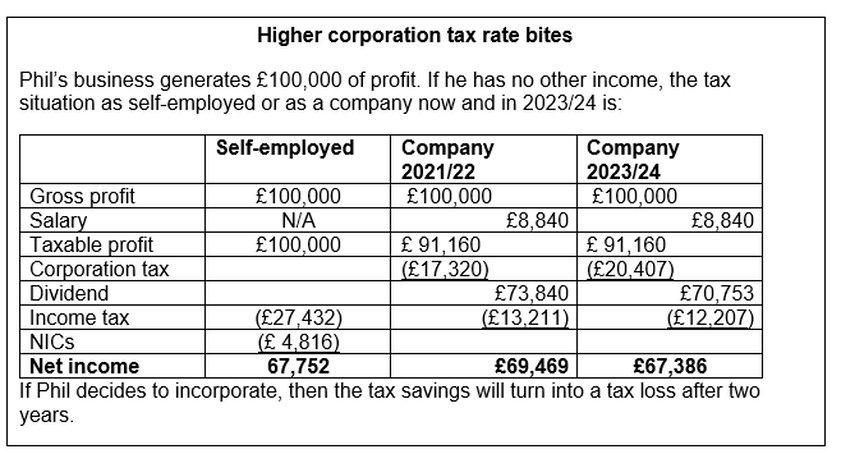

The planned increase in corporation tax has changed some of the mathematics on incorporation.

The Budget announced a significant change to corporation tax from 2023:

The decision on business structure should never be made based on tax alone as there are many other factors involved. However, the deferred tax changes announced in the Budget may tip the scales for some. As ever, advice based on your personal – and business – circumstances is essential.  As making tax digital extends to businesses and landlords from April 2023, the government is considering whether to increase the frequency of tax payments, both for the self-employed and companies.

The recently published consultation is part of the government’s ten-year strategy to build a modern tax administration system. Current problems The newly self-employed can go up to 22 months after commencement before their first tax bill, which can lead into debt. A similar problem arises if there is a large increase in profits from one year to the next. The consultation is only concerned with companies outside the quarterly instalment regime. The normal due date for such companies to pay their corporation tax is nine months and one day following the accounting period end, so again a significant time lag. It is all too easy for funds to have been spent if a year of high profits is followed by one with much lower income. Spreading payments One option likely to be available soon is an improvement to HMRC’s budget payment plan, making it easier for taxpayers to voluntarily budget for future tax payments. The consultation considers a move to quarterly or even monthly tax payments and points out that the majority of taxpayers already pay monthly or weekly under PAYE. However, a move to quarterly or monthly tax payments will mean more time spent on calculation and reporting, increasing the administrative burden on SMEs. More frequent tax payment also throws up other issues:

|

Photos from Pam loves pie, Homedust, wuestenigel, Patrick Cannon Tax Barrister, wuestenigel, Brett Jordan, wuestenigel, raisin_raisin, wuestenigel, SME Loans, Alexandre Prevot, Jirka Matousek, wuestenigel (CC BY 2.0), wuestenigel, Jirka Matousek, moneybright, aronbaker2, foundin_a_attic, QuoteInspector.com, wuestenigel, Kate#2112, Semtrio, Rawpixel Ltd, itmpa, GoSimpleTax, DPP Law, UC Davis College of Engineering, 401(K) 2013, REM Photo ~ Sketchy Internet, Chris Yarzab, focusonmore.com, focusonmore.com, willbuckner, EpicTop10.com, Tony Webster, wuestenigel, B Rosen, London Less Travelled